Please see this week’s market overview from eToro’s international analyst staff, which incorporates the most recent market information and the home funding view.

Most markets rose steadily in anticipation of Donald Trump’s presidency

Final week provided one thing for each kind of investor. Bond and small-cap traders discovered some aid in softer-than-expected inflation information, which brought on the US 10-year yield to fall from 4.76% to 4.62%. Worth traders have been happy with strong US financial institution earnings, all of which exceeded expectations. Progress and AI traders welcomed TSMC’s announcement of a deliberate enhance in capital expenditures for 2025 to roughly $40 billion, sparking hypothesis about which portion will fund a brand new state-of-the-art manufacturing unit within the US.

In the meantime, cryptocurrency fans have been astonished by the launch of a Trump memecoin, which skyrocketed to billions in market worth. This surge additionally lifted Bitcoin by 11% (to a brand new alltime excessive of $108,900), though it brought on a decline in lots of altcoins. China’s GDP development within the fourth quarter of 2024 rose to five.4%, arguably pushed by front-loaded exports looking for to keep away from increased tariffs underneath Trump’s presidency.

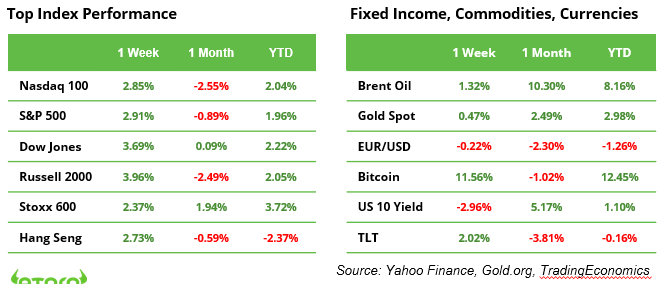

Main fairness indices closed the week in optimistic territory. The S&P 500 and Nasdaq 100 have been up by 3%, whereas the Dow Jones and Russell 2000 gained 3.7% and 4.0%, respectively. The European STOXX 600 and the China-focused Cling Seng additionally posted good points of two.4% and a pair of.7%, respectively. The UK FTSE 100 Index reached a brand new all-time excessive above 8,500 factors on Friday (see chart).

Macro Outlook for the week

This week in macro, traders will concentrate on the UK’s unemployment and wage development information, following final week’s lower-than-expected inflation, retail gross sales, and GDP figures. Markets are factoring in important charge cuts by the Financial institution of England in 2025, aiming to facilitate a gentle touchdown for the economic system.

Consideration may even flip to Germany’s financial sentiment index, as traders search indicators of bettering sentiment, significantly in gentle of current GDP information displaying the economic system contracted for a second consecutive yr. Notably, Germany stays the one main industrialized nation the place GDP per capita is projected to remain under 2019 ranges by means of 2025.

FTSE 100 Index reached a brand new all-time excessive above 8,500 factors on Friday

Who decides the destiny of the yen, the Financial institution of Japan or Donald Trump?

The yen and the euro have been dropping floor towards the greenback for months, with the dollar buoyed by a robust US economic system and the “Trump Commerce,” pushed by proposed tax cuts and looming tariffs.

Final week introduced some aid: EUR/USD climbed above 1.027, whereas USD/JPY fell 1% to 156.2. Yen merchants responded to Financial institution of Japan (BoJ) Governor Kazuo Ueda’s hints of a possible charge hike this Friday, following key inflation information due earlier that day.

Nonetheless, Japan’s choices stay restricted. Years of sluggish development and excessive public debt hold the economic system reliant on low rates of interest. Whereas the BoJ would possibly stabilise the yen, a serious rally appears unlikely. A weaker US greenback might show extra impactful than any BoJ coverage shift.

The yen’s destiny could in the end relaxation with Trump. His inauguration on Monday might form markets, with a robust greenback nonetheless the baseline underneath his “America First” agenda. Nonetheless, softer tariffs or fiscal insurance policies might weaken the greenback and provides the yen some respite.

Earnings season: large names reporting

The earnings season is coming into its essential second week, with seven of the world’s high 100 largest corporations reporting their 2024 This fall earnings (see under). Traders ought to recognise that some inventory costs could have been influenced by the upcoming presidential transition. In his last days, Joe Biden allotted $26 billion to wash power initiatives. In the meantime, Donald Trump has repeatedly said his intention to impose a 20% tariff on all items offered to the US, and a 60% tariff particularly on items from China. Execution orders, signed by Trump in his first week, might change federal insurance policies from the beginning and trigger surprising market actions.

Macro and earnings information releases

Macro

UK unemployment, Germany ZEW (22/1), Japan CPI, BoJ charge determination, International PMI (24/1)

Earnings

21 Jan. Netflix, Charles Schwab, 3M, United Airways

22 Jan. Procter & Gamble, Johnson & Johnson, GE Vernova, Amphenol

23 Jan. GE Aerospace, Texas Devices, American Airways

24 Jan. American Specific, Verizon, NextEra Power

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out taking into consideration any explicit recipient’s funding goals or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product will not be, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}